Singapore entrepot trading shipping declaration under ME scheme none Goods and Service tax

What is MES?

The Major Exporter Scheme (MES) is administered by the Inland Revenue Authority of Singapore (IRAS). This scheme is designed to alleviate the cash flow of companies that re-export a substantial amount of their imports.

Under normal rules, businesses have to pay the Goods and Services Tax (GST) of the goods imported to Singapore Customs, and subsequently obtain a refund from IRAS after the submission of their GST returns. This can hinder cash flow for businesses that export goods substantially as no GST is collected from the zero-rated supplies to off-set their initial cash outflow on their imports.

Companies approved under the MES can enjoy GST suspension for non-dutiable goods imported into Singapore, and on goods removed from a zero-GST warehouse.

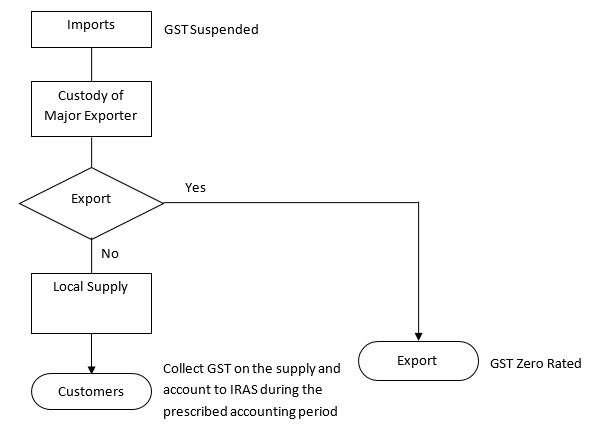

An overview of how the Major Exporter Scheme works:

Customs Permit Requirements

A Customs In-Non-Payment (Approved Premises / Schemes) permit must be obtained before removing the goods from the Free Trade Zone/entry point or the Zero-GST warehouse under the Major Exporter Scheme (MES). The place of receipt code should be declared as “ME”.

A Declaring Agent (DA) can only apply for permits for an approved MES person after the approved MES person has authorised that DA by using the online e-Service “Apply for Declaring Agents” at IRAS’ website.

For collection of postal parcels at SingPost Centre, a MES trader must present the Customs In-Non-Payment (Approved Premises / Schemes) permit before the parcel can be released without GST payment. Otherwise, the MES trader will have to pay GST on the parcel.

Read more about how to apply for import permits, GST suspension for goods removed from zero-GST warehouse under the MES and importing by postal or courier service.